IRVINE, Calif. / May 26, 2023 / Business Wire / The Masimo Corporation (“Masimo” or the “Company”) (Nasdaq: MASI) Board of Directors today issued a letter to stockholders in connection with its definitive proxy materials filed on May 24, 2023, and the Company’s Annual Meeting of Stockholders to be held on June 26, 2023. The letter outlines the management team and Board of Directors’ long track record of creating stockholder value, compelling strategy and responsive governance changes, in addition to detailing the risk Politan Capital Management (“Politan”) and its nominee Quentin Koffey pose to the Company’s strategy, principles and leadership. To protect stockholders’ investment and to ensure Masimo continues to create value, the Board encourages stockholders to vote FOR Masimo’s highly qualified director nominees, H Michael Cohen and Julie Shimer, Ph.D.

Find our definitive proxy materials and more information on why your vote is so important to the future of Masimo at www.KeepMasimoStrong.com. The full text of the Board’s letter to our stockholders can be found here:

Dear Fellow Masimo Shareholders:

Masimo was founded in 1989 by our current Chairman and CEO, Joe Kiani, and has become one of the most successful medical technology companies in the world by adhering to its guiding principles and developing breakthrough innovations that improve lives. The entire Masimo team and Board of Directors remain deeply committed to this approach, which has created incredible value and earned Masimo a sterling reputation with its customers, investors, and even competitors. Masimo has delivered exceptional shareholder returns from our initial public offering more than 15 years ago and over nearly all time periods. And as we look to the future, we intend to grow Masimo by continuing to develop and commercialize breakthrough products for both the hospital and the home.

Politan, a start-up activist hedge fund, and its founder and nominee Quentin Koffey, who has never even invested in, much less run, a medical technology company, want you to trust them to “fix” Masimo. Mr. Koffey’s track record and his representatives’ statements in court all indicate that Politan is ultimately seeking control of Masimo’s future. Yet their comments on Masimo’s strategy and performance show a dangerous ignorance of how we have achieved our success, the returns on our investments in innovation, and the rationale for our strategy, as well as a reckless willingness to distort the truth in pursuit of their agenda.

In the coming weeks, Politan and Mr. Koffey will deny they are seeking control and claim they only want greater oversight. Even taking that dubious claim at face value, Mr. Koffey is not qualified to deliver that. He lacks credibility and brings no industry experience, prior public company board service or diversity to Masimo. He has sued the Company and its current and former Board members and has refused to collaborate with the Board to appoint two new directors independent of both Masimo and Politan for the benefit of all shareholders, insisting on a seat for himself despite clearly not meeting the Board’s criteria for new directors. He has refused to even provide dates for Masimo’s Nominating Committee to interview Michelle Brennan, the other Politan nominee.

The risks of giving Mr. Koffey a foothold in the boardroom so he can try to scrap the approach that has served Masimo and its shareholders well for its entire history are immense. Masimo is not an industry laggard that has nowhere to go but up. Masimo is the market leader in non-invasive monitoring, with robust plans to continue leading and transforming healthcare and consumer health.

At the upcoming Annual Meeting, you have a critical choice to make regarding your investment in the future of Masimo. The Company’s mission, strategy and guiding principles are all at stake.

Here are five important reasons why you should vote “FOR” Masimo’s director nominees―Julie Shimer, Ph.D., and H Michael Cohen―on the WHITE proxy card today:

For 34 years, whether public or private, Masimo has delivered for its shareholders, and under the current strategy, the Company is well-positioned to continue creating shareholder value. Mr. Koffey’s candidacy threatens Masimo’s strategy, principles and leadership. As our actions and plans show, your Board brings experienced oversight, new ideas and diverse and ethical perspectives. There is no need to risk derailing Masimo’s progress to advance Quentin Koffey’s personal self-interest and hidden agenda.

LONG TRACK RECORD OF OUTPERFORMANCE AND STRATEGIC EXECUTION

Since its 2007 IPO through May 1, 2023, when Politan nominated its director candidates, Masimo’s stock has returned more than 1,000 percent for shareholders, more than triple that of the S&P 500 Index, more than double that of the Nasdaq Composite Index and nearly double that of the Dow Jones U.S. Select Medical Equipment Index (the “Medical Devices Index”) during the same period. Indeed, Masimo has outperformed relevant comparisons for almost all time periods, both short-term and long-term. All the while, Masimo has been a beacon of hope for clinicians and patients, helping clinicians save and improve countless lives.

Total Shareholder Return

| From | To | Masimo | S&P 500 | NASDAQ Composite | Medical Devices Index |

Various Time Periods |

|

|

|

| ||

YTD | 1/3/2023 | 5/1/2023 | 29% | 10% | 18% | 8% |

From 1 Year Ago | 5/2/2022 | 5/1/2023 | 59% | 2% | (2%) | 4% |

From 3 Years Ago | 5/1/2020 | 5/1/2023 | (13%) | 54% | 45% | 38% |

From 5 Years Ago | 5/1/2018 | 5/1/2023 | 106% | 71% | 79% | 85% |

From 10 Years Ago | 5/1/2013 | 5/1/2023 | 852% | 219% | 311% | 396% |

|

|

|

|

|

|

|

Key Events |

|

|

|

|

|

|

Since Investor Day | 12/12/2022 | 5/1/2023 | 32% | 5% | 10% | 6% |

Since IPO | 8/7/2007 | 5/1/2023 | 1,012% | 288% | 460% | 568% |

The Company has achieved these strong returns for shareholders through sustained improvements in operating performance and disciplined capital allocation that have driven profitable, above-market growth. Under the Company’s previous long-term strategic plan announced at its 2017 Investor Day and overseen by the current Board, Masimo delivered total shareholder returns of 243 percent through December 31, 2021, compared to 109 percent for the S&P 500 Index, 156 percent for the Nasdaq Composite Index and 150 percent for the Medical Devices Index.

[See image]

Across that period, Masimo recorded the following operating results, delivering on its promises by exceeding targets set under the 2017 plan:

______________

(1) Market estimates based upon internal data, iData & Futuresource.

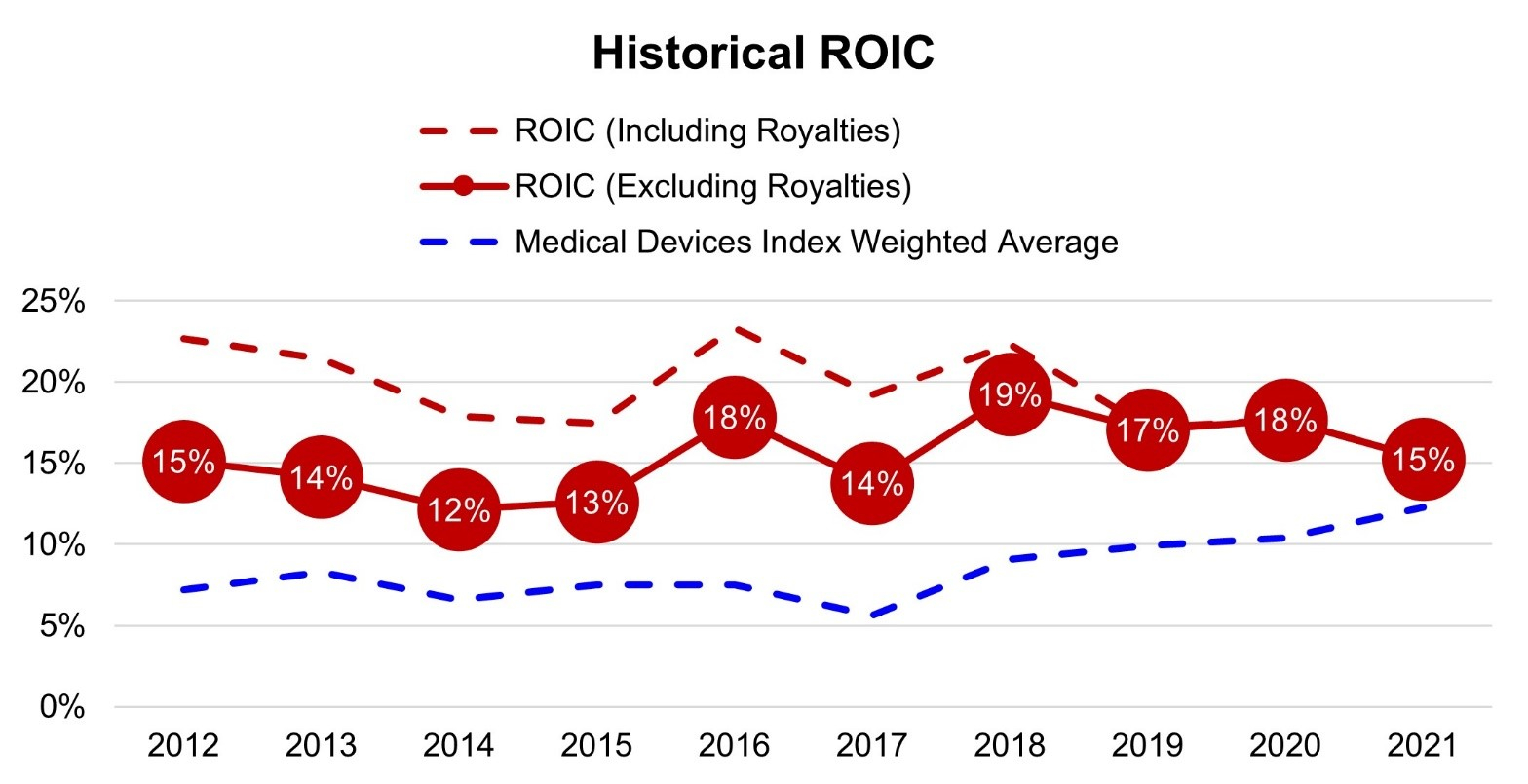

During the same period, the Company’s innovation-focused strategy and rigorous capital allocation process sustained ROIC at levels well above the medical device industry and Masimo’s prior performance, even as the Company expanded into new and adjacent markets.

[See image]

RIGHT STRATEGY FOR THE FUTURE

Masimo’s strategic plan sets the stage for the Company to continue to deliver superior shareholder returns by strengthening the existing professional healthcare franchise and creating new long-term growth opportunities in the telemonitoring, consumer health and hearables markets.

The acquisition of Sound United and the creation of Masimo Consumer have opened these markets to the Company without a dilutive, multi-year investment. The management team and Board thoroughly assessed both organic and inorganic strategies to enter these markets and evaluated more than 200 potential acquisition targets before determining that Sound United offered the best prospects for long-term value creation. By providing immediate sales and distribution scale and opportunities for synergistic tech transfer, product development and marketing efforts, the acquisition allows Masimo to leverage the value of its unique technologies and capabilities in the $20 billion telemonitoring, $50 billion consumer health, and $85 billion hearables markets.

At the same time, shifting physician and patient preferences in the wake of the Covid pandemic and the pressure to reduce the cost of care have revealed significant unmet needs and new opportunities in the professional healthcare market that merit continued innovation and investment. Strengthening our capabilities to monitor patients at home and seamlessly connect them and their data to providers increases the appeal of our healthcare solutions in a rapidly evolving market. This approach mirrors our past successes driving adoption of SET® by entering and innovating in adjacent markets. Masimo couldn’t have continued to gain market share from a powerful incumbent with pricing advantages and bundling practices with a much broader product portfolio if it had relied on SET® pulse oximetry alone. Rainbow®, Hospital AutomationTM, Radius PPG®, and other advanced technologies have given hospitals further reasons to standardize on Masimo SET®. By pursuing consumer health applications for its core technologies, Masimo is also bolstering its core healthcare business.

Our strategy creates value for patients, clinicians, hospitals and shareholders by bringing Masimo’s differentiated and clinically superior technologies, proven track record of innovation and customer-driven approach to product development to new markets, while also enhancing the Company’s ability to serve patients and providers regardless of care setting. With management’s track record of strong execution, Masimo is well-positioned to drive sustainable revenue and earnings growth.

We have also set clear guardrails in our pursuit of this strategy, beginning with the reasonable and accretive purchase price for Sound United and our modest use of financial leverage. We have publicly explained our commitment to exit the business in three years if our consumer health products do not gain traction in the market. We have limited our incremental spending on consumer product launches to one percent of revenue and are intensely focused on leveraging Sound United’s existing 20,000 points of distribution and 500 consumer sales and marketing professionals to drive consumer adoption.

As disclosed at the Investor Day on December 13, 2022, Masimo has issued conservative long-range financial targets for 2023-2028 that contemplate profitable long-term growth:

Notably, these targets include Masimo’s product portfolio as of Investor Day but do not reflect the potential benefits of future consumer-focused products that are rolling out beginning in the second half of 2023.

Masimo has already made significant progress advancing its strategy, as more fully detailed at the Investor Day and on the Q4 2022 and Q1 2023 earnings calls. Masimo has won a number of hospital customers for the W1™ advanced health tracking watch for telemonitoring, launched the Stork baby monitor and Opioid Halo opioid overdose prevention and alert system, and has begun the presale of the Masimo Freedom health-tracking smartwatch with Android OS. So far, the reaction of our existing hospital customers to our plans has been remarkable because they see how this could benefit them and their patients. We will soon find out if consumers agree.

Since management unveiled the strategy at the Investor Day through May 1, 2023, the day before Politan publicly announced its nominees for the Board, Masimo’s stock has returned 32 percent, compared to 5 percent for the S&P 500 Index, 10 percent for the Nasdaq Composite Index and 6 percent for the Medical Device Index. This outperformance has substantially closed the valuation gap between Masimo and its peers that opened following the Sound United acquisition.2 We believe the strong market response demonstrates the growing conviction that this strategy maximizes the value of the Company and validates the potential return on investment of the Sound United acquisition.

[See image]

______________

(2) Peer index reflects average of premium / discount of Masimo AV / NTM EBITDA to select peers (Align, Edwards Life Sciences, Intuitive Surgical, Resmed)

KOFFEY HAS BEEN UNPRINCIPLED AND SELF-SERVING IN HIS ENGAGEMENT

Unlike most activist investors, Politan did not come to the table offering business ideas or even a point of view. Until this week, Politan and Mr. Koffey did not share any actionable recommendation or guidance for the Company other than demanding two board seats, including one for himself. Indeed, Mr. Koffey even predicated his views about the Company on its response to his demand, stating directly to the Company that he would be management’s “biggest cheerleader” if added to the Board and would wage a proxy contest against the Company if not.

This unprincipled statement contradicts Mr. Koffey’s long track record of instigating CEO change at his targets. In all but one of his past campaigns, the CEO has been replaced within one year of the campaign.3 Mr. Koffey’s attacks on the validity of Mr. Kiani’s eight-year-old employment agreement indicate his end goal is the same in this case. Indeed, in the litigation filed by Politan against Masimo’s current and former directors, Politan’s attorney gave the court an indication of Politan’s true intentions:

“[Y]es, we may be able to get two seats, but nobody going into this election will know if a third seat and potential control is available. And the [Politan] candidates are telling us that's important to them.”

We believe Mr. Koffey is seeking control of the Company. He doesn’t want to say as much to Masimo shareholders because most will not agree it is a risk worth taking. CEO change would have a devastating impact on Masimo and its ability to retain the core engineering and management teams, many of whom have worked closely with Mr. Kiani for more than a decade, some for three decades.

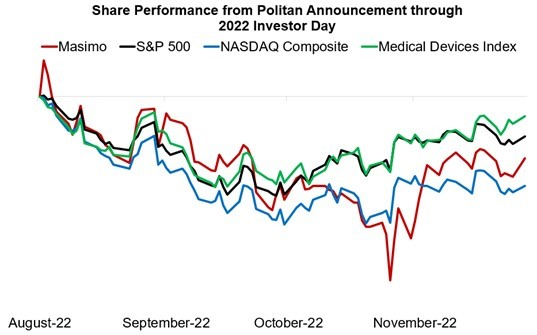

With no business ideas, no public plan and a history of CEO change, Politan’s campaign was poorly received by the market. From the day prior to Politan’s first public announcement of its ownership stake on August 16, 2022, to Masimo’s Investor Day, Masimo’s stock price declined 10 percent, compared to a 7 percent decline for the S&P 500 Index, a 15 percent decline for the Nasdaq Composite Index and a 3 percent decline for the Medical Devices Index. The stock’s outperformance following the Investor Day is a powerful reminder of the value of Masimo’s strategic vision and the critical importance of not allowing Mr. Koffey to derail the Company’s momentum.

______________

(3) Includes past campaigns publicly associated with Quentin Koffey at Politan, D.E. Shaw and Senator Investment Group and excludes Masimo and hostile bid campaigns; CEO replacement includes cases where a CEO departure was announced within 1 year of the public campaign announcement

[See image]

Despite Politan’s unprincipled behavior and failure to produce business ideas or even a positive market reaction to its presence, we gave Mr. Koffey multiple opportunities to work with us to identify and add to the Board two mutually agreeable directors who are independent of both Masimo and Politan. Instead of accepting this clear path to strengthening the Board as Politan claims to desire, Politan refused to engage unless we acquiesced to its self-serving demand that Mr. Koffey be added to the Board. Politan has so far refused to provide available dates for Masimo’s Nominating Committee to interview Michelle Brennan, Politan’s other nominee.

Politan’s unprincipled approach, hidden agenda and unwillingness to cooperate to find outside directors more qualified than Mr. Koffey clearly demonstrate that its campaign is not about delivering the best outcome for Masimo shareholders but about laying the groundwork to oust Mr. Kiani and getting Quentin Koffey his first public company board seat, regardless of his qualifications.

MASIMO’S NOMINEES ARE CLEARLY SUPERIOR TO QUENTIN KOFFEY

On that account, the facts are that Mr. Koffey is a woefully unqualified candidate for Masimo’s Board.

Mr. Koffey does not meet a single criterion for director candidates set out by the Board and would never have made it through an independent process.

While his lack of credentials speaks volumes on its own, Mr. Koffey’s commentary shows he has barely been paying attention since establishing his position in Masimo. Putting aside the factual errors and inaccuracies – which we will correct separately – his critique of the Company issued this week reflects a fundamental misunderstanding of Masimo’s business, industry and history.

We are hardly surprised by Mr. Koffey’s ignorance, willful or otherwise, on these matters. Despite Politan’s stated interest in Masimo, they have repeatedly refused to engage with management to learn more about the Company and its business strategies.

Mr. Koffey himself can’t even explain why he’d make a good candidate for Masimo’s Board. When asked about his demand to be installed as a Board member during his first meeting with the Company in September 2022 and in subsequent meetings, Mr. Koffey offered no reason beyond Politan’s standing as a large shareholder. His letter shows he has not advanced his case.

By contrast, our current independent directors all have highly relevant strategic, operational, financial, and investing experience in healthcare and medical devices that has allowed them to exercise the proper level of oversight. Dr. Shimer and Mr. Cohen, the current directors standing for election in 2023, both have exceptionally deep healthcare industry experience and were supported by more than 95 percent of voting shareholders in past elections. Dr. Shimer has significant experience as a CEO and director of numerous medical device and consumer-facing technology companies, while Mr. Cohen has more than 30 years of experience in healthcare investment banking and equity research covering medical technology, devices and related industries.

Along with wasting a valuable Board seat on a candidate with no complementary skills or experience, Mr. Koffey’s track record of instigating CEO change and his self-interested and uniquely adversarial posture towards the Company threaten to mire the boardroom in dysfunction and chaos and further exacerbate the potential for harm to Masimo and its shareholders.

OUR EMBRACE OF POSITIVE SHAREHOLDER-DRIVEN CHANGE

Taking this risk is needless. We have consistently solicited and responded to constructive input from Masimo’s shareholders as part of our longstanding shareholder outreach program. In the past, the Board has supported and implemented many ideas proposed by shareholders, including establishing an OUS headquarters, changing our executive pay and contracting practices and limiting the tenure of independent Board members. Most recently, on March 23, 2023, Masimo announced significant changes to its governance policies as a result of a review process that involved meetings with shareholders representing more than 50 percent of the Company’s outstanding shares, including:

These changes show that we respect the wishes of our shareholders and understand the need to ensure that you have confidence in the integrity of our decision-making processes. Just as importantly, we remain deeply committed to gathering and acting on shareholder feedback, and these changes support our continued ability to do so.

One point consistently raised by shareholders in our recent engagement meetings was the need for a larger and more diverse Board. Masimo has traditionally had seven directors, but due to retirements and Covid, the Board now has five. Shareholders also agreed that extensive consumer, payer/provider, or government policy experience are important qualifications for new directors. Our proposal to expand the Board from five to seven directors and to identify two new, highly qualified and complementary independent directors with the support of an external advisory firm is a direct response to that feedback.

To act promptly on this, the Board is actively engaged with an independent third-party search firm to develop a robust pipeline of highly qualified director candidates. In addition, the Board welcomes suggestions for potential director candidates from all its shareholders, including Politan. On multiple occasions, we have directly expressed to Politan our willingness to work together to identify two new, mutually agreeable directors who are independent of both Masimo and Politan to join the expanded Board, and Politan has refused to cooperate at every turn.

YOUR VOTE ON THE WHITE PROXY CARD IS CRITICAL

Your vote for our nominees helps maintain Masimo’s momentum and ensures that the Company’s ability to create shareholder value, improve lives, improve patient outcomes, reduce the cost of care, and take noninvasive monitoring to new sites and applications, is not disrupted.

We urge you to use the enclosed WHITE proxy card to vote today “FOR” all Masimo’s director nominees: Julie Shimer, Ph.D., and H Michael Cohen.

Electing Quentin Koffey to the Board threatens Masimo’s mission, principles, strategy and leadership and jeopardizes the potential of your investment in Masimo. Please do not vote using any blue proxy card you may receive from Politan. Any vote on the blue proxy card will revoke your prior vote on a WHITE proxy card, and only your latest-dated proxy counts.

Masimo’s Board has been unified and unwavering in its commitment to act in the best interests of all shareholders. We look forward to continuing our fruitful engagement with you as we work to deliver enhanced shareholder value in the years ahead.

Thank you for your continued support,

Masimo Board of Directors

About Masimo

Masimo (Nasdaq: MASI) is a global technology company that develops and produces a wide array of industry-leading monitoring technologies, including innovative measurements, sensors, patient monitors, and automation and connectivity solutions. In addition, Masimo Consumer Audio is home to eight legendary audio brands, including Bowers & Wilkins®, Denon®, Marantz®, and Polk Audio®. Our mission is to improve life, improve patient outcomes and reduce the cost of care. Masimo SET® Measure-through Motion and Low Perfusion™ pulse oximetry, introduced in 1995, has been shown in over 100 independent and objective studies to outperform other pulse oximetry technologies. Masimo SET® has also been shown to help clinicians reduce severe retinopathy of prematurity in neonates, improve CCHD screening in newborns, and, when used for continuous monitoring with Masimo Patient SafetyNet™ in post-surgical wards, reduce rapid response team activations, ICU transfers, and costs. Masimo SET® is estimated to be used on more than 200 million patients in leading hospitals and other healthcare settings around the world, and is the primary pulse oximetry at 9 of the top 10 hospitals as ranked in the 2022-23 U.S. News and World Report Best Hospitals Honor Roll. In 2005, Masimo introduced rainbow® Pulse CO-Oximetry technology, allowing noninvasive and continuous monitoring of blood constituents that previously could only be measured invasively, including total hemoglobin (SpHb®), oxygen content (SpOC™), carboxyhemoglobin (SpCO®), methemoglobin (SpMet®), Pleth Variability Index (PVi®), RPVi™ (rainbow® PVi), and Oxygen Reserve Index (ORi™). In 2013, Masimo introduced the Root® Patient Monitoring and Connectivity Platform, built from the ground up to be as flexible and expandable as possible to facilitate the addition of other Masimo and third-party monitoring technologies; key Masimo additions include Next Generation SedLine® Brain Function Monitoring, O3® Regional Oximetry, and ISA™ Capnography with NomoLine® sampling lines. Masimo’s family of continuous and spot-check monitoring Pulse CO-Oximeters® includes devices designed for use in a variety of clinical and non-clinical scenarios, including tetherless, wearable technology, such as Radius-7®, Radius PPG® and Radius VSM™, portable devices like Rad-67®, fingertip pulse oximeters like MightySat® Rx, and devices available for use both in the hospital and at home, such as Rad-97®. Masimo hospital and home automation and connectivity solutions are centered around the Masimo Hospital Automation™ platform, and include Iris® Gateway, iSirona™, Patient SafetyNet, Replica®, Halo ION®, UniView®, UniView :60™, and Masimo SafetyNet®. Its growing portfolio of health and wellness solutions includes Radius T® and Masimo W1™ watch. Additional information about Masimo and its products may be found at www.masimo.com. Published clinical studies on Masimo products can be found at www.masimo.com/evidence/featured-studies/feature/.

ORi and RPVi have not received FDA 510(k) clearance and are not available for sale in the United States. The use of the trademark Patient SafetyNet is under license from University HealthSystem Consortium.

Forward-Looking Statements

All statements other than statements of historical facts included in this press release that address activities, events or developments that we expect, believe or anticipate will or may occur in the future are forward-looking statements including, in particular, the statements about our expectations for full-year 2023 financial guidance; the interest in our W1™ watch and upcoming innovations; our long-term outlook; demand for our products; anticipated revenue and earnings growth; our financial condition, results of operations and business generally; expectations regarding our ability to design and deliver innovative new noninvasive technologies and reduce the cost of care; our ability to address supply chain challenges; anticipated benefits from our acquisition of Sound United; and demand for our products and technologies; including with respect to revenue, revenue growth and constant currency revenue growth, gross margin, operating margin, GAAP earnings per diluted share, non-GAAP earnings per diluted share, estimated tax rate and year-over-year currency headwinds; our long-term outlook; our ability to continue in our leadership in delivering innovative solutions to clinicians and patients worldwide; anticipated revenue and earnings growth. These forward-looking statements are based on management’s current expectations and beliefs and are subject to uncertainties and factors, all of which are difficult to predict and many of which are beyond our control and could cause actual results to differ materially and adversely from those described in the forward-looking statements. These risks include, but are not limited to, those related to: our dependence on Masimo SET® and Masimo rainbow SET™ products and technologies for substantially all of our revenue; any failure in protecting our intellectual property exposure to competitors’ assertions of intellectual property claims; the highly competitive nature of the markets in which we sell our products and technologies; any failure to continue developing innovative products and technologies; the lack of acceptance of any of our current or future products and technologies; obtaining regulatory approval of our current and future products and technologies; the risk that the implementation of our international realignment will not continue to produce anticipated operational and financial benefits, including a continued lower effective tax rate; the loss of our customers; the failure to retain and recruit senior management; product liability claims exposure; a failure to obtain expected returns from the amount of intangible assets we have recorded; the maintenance of our brand; the amount and type of equity awards that we may grant to employees and service providers in the future; our ongoing litigation and related matters; risks related to global economic and marketplace uncertainties related to the impact of the COVID-19 pandemic; and other factors discussed in the “Risk Factors” section of our most recent periodic reports filed with the Securities and Exchange Commission (“SEC”), including our most recent Form 10-K and Form 10-Q, all of which you may obtain for free on the SEC’s website at www.sec.gov. Although we believe that the expectations reflected in our forward-looking statements are reasonable, we do not know whether our expectations will prove correct. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof, even if subsequently made available by us on our website or otherwise. We do not undertake any obligation to update, amend or clarify these forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Additional Information Regarding The Annual Meeting of Stockholders Currently Expected to Be Held on June 26, 2023 and Where to Find It

Masimo has filed a definitive proxy statement containing a form of WHITE proxy card with the SEC in connection with its solicitation of proxies for its 2023 Annual Meeting. MASIMO’S SHAREHOLDERS ARE STRONGLY ENCOURAGED TO READ THE DEFINITIVE PROXY STATEMENT (AND ANY AMENDMENTS AND SUPPLEMENTS THERETO) AND ACCOMPANYING WHITE PROXY CARD AS THEY WILL CONTAIN OR CONTAIN IMPORTANT INFORMATION. Shareholders may obtain the proxy statement, any amendments or supplements to the proxy statement and other documents as and when filed by Masimo with the SEC without charge from the SEC’s website at www.sec.gov.

Certain Information Regarding Participants

Masimo, its directors and certain of its executive officers may be deemed to be participants in connection with the solicitation of proxies from Masimo’s shareholders in connection with the matters to be considered at the 2023 Annual Meeting. Information regarding the ownership of Masimo’s directors and executive officers in Masimo common shares is included in Masimo’s definitive proxy statement, which can be found through the SEC’s website at www.sec.gov. To the extent holdings of Masimo’s securities by directors or executive officers have changed since the amounts set forth in the definitive proxy statement, such changes have been or will be reflected on SEC filings filed by the applicable individuals on Forms 3, 4, and 5, which can be found through the SEC’s website at www.sec.gov. These documents can be obtained free of charge from the sources indicated above.

Masimo, SET, Signal Extraction Technology, Improving Patient Outcome and Reducing Cost of Care... by Taking Noninvasive Monitoring to New Sites and Applications, rainbow, SpHb, SpOC, SpCO, SpMet, PVI and ORI are trademarks or registered trademarks of Masimo Corporation.

| Last Trade: | US$169.74 |

| Daily Change: | -1.23 -0.72 |

| Daily Volume: | 115,774 |

| Market Cap: | US$9.090B |

November 26, 2024 November 05, 2024 October 29, 2024 September 25, 2024 | |

ClearPoint Neuro is a global therapy-enabling platform company providing stereotactic navigation and delivery to the brain. Applications of our ClearPoint Neuro Navigation System include electrode lead placement, placement of catheters, and biopsy. The platform has FDA clearance and is...

CLICK TO LEARN MORE

Chimerix is on a mission to develop medicines that meaningfully improve and extend the lives of patients facing deadly diseases. The company is devoted to filling gaps in the treatment paradigm. Chimerix’s most advanced clinical-stage program is in development for H3 K27M-mutant glioma....

CLICK TO LEARN MORE